The Japanese Market - Finally reached escape velocity or still a victim of the country’s historic deflationary doom-loop?

There was a time when the more sanguine among investors used to divide world markets into four broad categories: developed and emerging markets, Argentina and Japan.

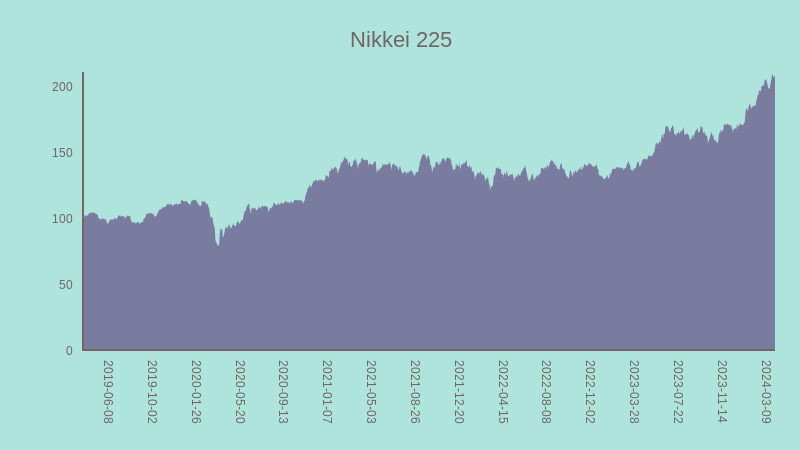

But amid so much other market news, two unusual things have happened recently in Japan: in February, the Nikkei 225 finally surpassed the peak reached 34 years ago. The following month, the Bank of Japan ended its negative interest rate policy and raised interest rates for the first time in 17 years. After years of entrenched deflation and stagnant economic conditions, prices in Japan started rising in spring 2022, finally spiked into action by the shocks of the COVID Pandemic and Russia’s invasion of Ukraine.

For years, global investors have shunned the Japanese stock market. Big Japanese companies tended to retain large cross-holdings in other listed companies and around half traded below the book value of their net assets. Shareholder interests never featured near the top of management's concerns. Ordinary Japanese investors dumped domestic shares after the crash of 1989 and held over half their financial assets in cash. Although that cash might have been earning zero at the bank, there was no urgency ever to take equity risk if, with deflation, this capital was not losing any real value or intrinsic purchasing power. With an ageing demographic more inclined to save than to invest, this tendency became entrenched.

Now, with inflation picking up - core inflation reached a mighty 2.8% annualised in Feb – and once docile workers demand higher pay amid demographic labour shortages, savers and investors are beginning to review their options. As a result, could Japanese equities be entering a bull run, driven by narratives about corporate behaviour returning to global norms?

While the Tokyo Stock Exchange has been pressuring companies to prioritise returns on equity and other shareholder considerations, the government too has been doing their bit with the introduction of a tax-incentivised Nippon Individual Savings Account or ‘NISA’. As of December 2023, Japanese savers had opened an impressive 21.3 million accounts.

In base currency, the TOPIX 500 has actually been outperforming the S&P 500, with similar earnings growth, but on much lower valuations. Following the recent rally, we have been gradually switching out of a core fund holding in higher risk portfolios, CC Japan Income & Growth Trust (+35% for the twelve months to end-March) and into the JP Morgan Japan Fund, taking advantage of the attractive discount still available there. This fund, too, has been enjoying something of a re-rating (+18.5% to end-Mar.) and Nicholas Weindling, its manager who is based in Tokyo, was distinctly bullish about the prospects for many of the holdings in his fund during a call with us recently.

Nor are investors at lower risk scales missing out. Within our Esk Global Equity Fund, held more widely across upper-lower and moderate risk scales, significant holdings in such as Shin-Etsu (chemicals), Chugai Pharmaceuticals, Sony Group, Sumitomo Mitsui (financial conglomerate) and Nomura (banking), now comprise nearly 10% of the portfolio.

There is still a division between those who expect Japan to revert to the mean and those who believe the Japanese valuations can now safely be compared to those elsewhere. But for the moment, we remain happy to ride the wave via the high-quality companies held in Esk and the two sector-leading investment trusts we currently favour in CH portfolios.

Note: The chart shows the Nikkei 225 Index's performance over five years, starting from April 2019, using data from Bloomberg. Since the author wrote this piece, the Nikkei 225 has fallen, like the rest of the world indices, largely due to escalating events in the Middle East.

Previous articles in this series

Markets in a moment - March 2024

Markets in a moment - February 2024

Markets in a moment - January 2024

Important Information

The contents of this article are for information purposes only and do not constitute advice or a personal recommendation. Investors are advised to seek professional advice before entering into any investment arrangements.

Please also note that the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?