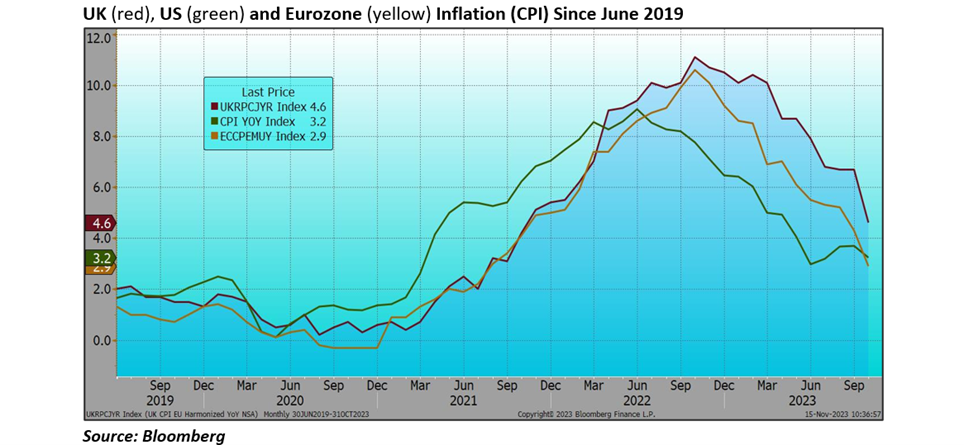

Hopefully, this will be the last time that we show this chart for a while. Inflation has continued to moderate and UK inflation has moved much more in-line with international rates: Returning to Earth (right)...

Of course, these inflation rates are still too high. We must expect multiple warnings from the Bank of England (along with the Federal Reserve and European Central Bank) that the inflation dragon is not yet slain and rates may well have to go higher yet. But these central banks are all now on ‘hold’ and the bond markets have moved from a mid-October panic over the new supply of government debt (they all need to raise lots of money), to a conviction that we have seen the peak in rates.

Conditions have been volatile, but it is worth a quick look at the change in yields over this period as they are stark, first the short-dated yields:

|

Two-Year Bond Yield: |

Today |

19th October |

Peak Rate |

|

U.K. |

4.5% |

5.0% |

Early July at 5.5% |

|

U.S. |

4.9% |

5.2% |

19th October was the peak |

|

Germany |

3.0% |

3.2% |

Early March at 3.3% |

And the ten-year rates:

|

Ten-Year Bond Yield: |

Today |

19th October |

Peak Rate |

|

U.K. |

4.15% |

4.7% |

Mid-August at 4.75% |

|

U.S. |

4.5% |

5.0% |

19th October was the peak |

|

Germany |

2.6% |

2.9% |

Early October at 2.95% |

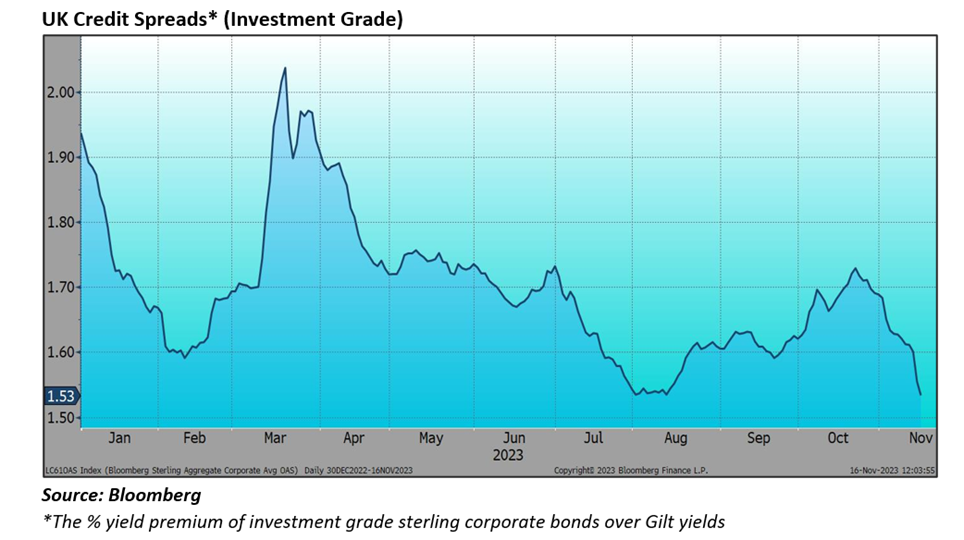

Of course, this translates into gains for Gilts and the other sovereign bond markets over this period, recovering some of the losses of the first half (though longer-dated issues have quite a way to go yet). Credit spreads have also closed back in again, taking them back to the lows for the year, right.

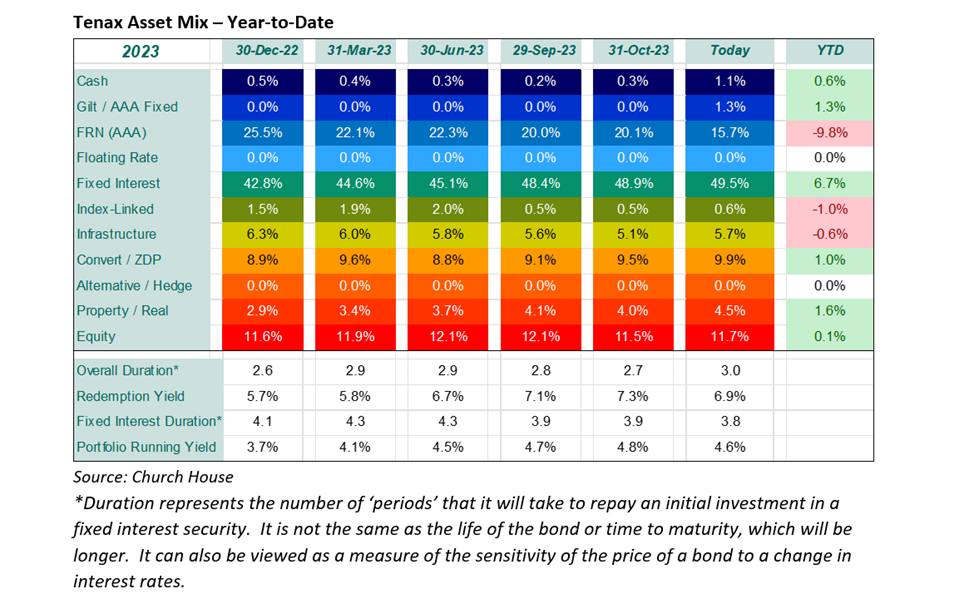

As the 'Tenax Asset Mix' table (right, below) shows, we have stepped-up the pace of the move from floating rate (FRN) issues to fixed, keen to lock-in current short-term rates. The FRNs have served the Fund exceptionally well, paying a steadily increasing rate of interest while maintaining their capital value, now it is time to move on. As we reduce the FRN exposure the overall duration will increase, as above, while the redemption yield from the 2/3 of the portfolio in fixed and floating investments has edged down with the increase in prices (we do not include the redemption yields from the convertible and index-linked issue in the portfolio in this figure).

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?